California home buyers typically encounter closing costs when buying a home. These are the various…

How Much Do Home Appraisals Cost in California, and Other FAQs

In a previous article, we explained how the home appraisal process works here in the state of California. Today, we will look at how much an appraisal actually costs, on average.

In California, a standard appraisal typically ranges from $400 – $600. This average has been updated for 2025 based on the latest data. But the cost can vary due to a wide range of factors, including these.

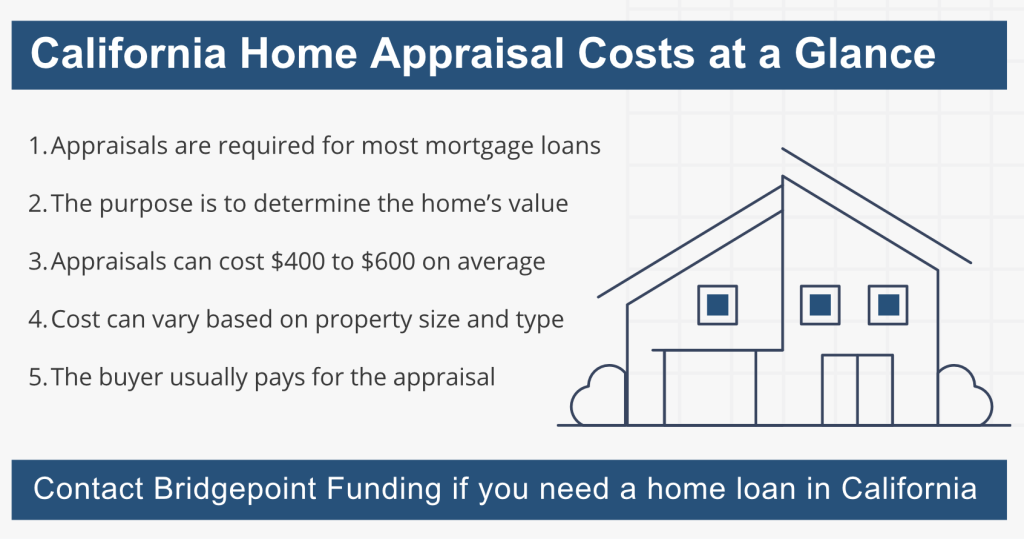

Here are five things to know about this subject right up front:

- Standard Requirement: If you’ll be using a mortgage loan to buy a home, the property will have to be appraised to determine its value. This is true for FHA, VA, and conventional loans.

- Average Cost: A standard home appraisal in the state of California typically costs between $400 – $600, on average. But it can exceed that range in rarer cases.

- Pricing Factors: The cost can vary based on factors such as property size, location, the appraiser’s expertise, property condition, demand, and urgency.

- Who Pays: In most cases, the home buyer will pay for the appraisal when using a mortgage loan. But the cost can sometimes be negotiated between buyer and seller.

- Appraisal Process: The lender orders an appraisal, the appraiser evaluates the home and comparable sales, and the final report determines if the loan can proceed.

Average Cost of a Home Appraisal in California

A home appraisal is an unbiased estimate of the market value of a home. It is performed by a licensed appraiser who considers factors such as the property’s location, condition, size, features, and recent sales in the area.

In California, the average cost of a home appraisal for a typical property ranges from $400 – $600.

Here are some of the factors that can determine the cost of an appraisal:

- Property size and type: Larger homes or more complex property types often require more time and effort to evaluate, which can lead to higher appraisal costs.

- Location: The geographic location of the property matters as well. Appraisal costs can vary by region, with urban areas typically being more expensive to appraise due to higher demand and cost of living.

- Expertise: The experience and qualifications of the appraiser can influence the cost of a home appraisal in California. Highly experienced and sought-after appraisers might charge more for their services.

- Property condition: The condition of the property plays a role. Properties with damage or other issues often require a more detailed inspection, which can increase the cost.

- Demand: Appraisals may cost more during peak times of year, such as the spring and summer months. This is because appraisers are typically busier during these times and may charge a premium for their services.

- Urgency: If you need a rush appraisal, expect to pay more. Appraisers often charge extra for expedited services. But in a typical home-buying scenario, this is usually not a factor.

When you first apply for a mortgage loan in California, you’ll be given an estimate of all costs including the appraisal fee. So there shouldn’t be any surprises along the way.

Who Pays for It, and When?

In California, the buyer is usually responsible for covering the cost of the home appraisal. (At least in cases where a mortgage loan is being used.) The buyer’s lender will require an appraisal to ensure that the property value matches the loan amount.

The cost can be paid when the appraisal is conducted, or rolled into the closing costs. This can vary from one lender to the next, depending on the arrangement and relationship they have with their preferred appraisers.

Like many aspects of a real estate transaction, the payment of the appraisal can be negotiated between the buyer and seller. In a slower market, a seller might be willing to cover the cost of the appraisal.

Homeowners sometimes order their own appraisals, prior to listing their homes for sale. They do this to find out what the property might be worth in the current market. This allows the seller to set a realistic asking price, increasing the chance for a sale.

In the case of mortgage refinancing (when a person replaces their existing home loan with a new one), the homeowner typically pays for the property appraisal.

The takeaway: In a typical real estate transaction, the home buyer pays for the appraisal at the time the service is actually performed. But this can vary, so ask about it upfront.

How the Process Works, at a Glance

Let’s zoom out for a moment and look at the broader process. Here’s a simplified example of how an appraisal works in California:

- A buyer and seller agree on a purchase price for a home.

- The buyer’s lender orders an appraisal to determine the current market value.

- The appraiser evaluates the home and collects information about its features and condition.

- The appraiser also researches recent sales of comparable homes in the same area.

- The appraiser then writes a report that states their opinion of the home’s market value.

If the appraised value is equal to or greater than the purchase price, the mortgage lender will likely approve the loan.

However, if the appraised value is lower than the purchase price, the buyer and seller may need to renegotiate the price. Or the buyer might need to come up with more cash for a down payment, or simply find another property.

Learn More About the Appraisal Process

We have created one of the largest libraries of educational articles geared toward home buyers in California. Many of them focus on the home appraisal process in particular, including the following topics:

Why Mortgage Loans Require an Appraisal

In California, nearly all purchase loans require a property appraisal prior to closing. This is true for FHA, VA and conventional mortgage products alike. This article explains why they are required and how it relates to you, as a home buyer.

How a Home Appraisal Contingency Works

In a real estate context, a “contingency” is a condition that must be met for the transaction to proceed. An appraisal contingency, for example, allows you to back out of the deal if the house appraises for less than the amount you’ve agreed to pay.

Difference Between Appraisals and Inspections

First-time home buyers in California sometimes confuse the home appraisal with the inspection. But they are two different things. One focuses on the market value of the house, while the other focuses on the condition of the property.

How Do Home Appraisers Determine Value?

Appraisers use a variety of tools and metrics to determine the market value of a particular property, and this includes using comparable sales or “comps.” This article provides an in-depth look at the valuation process.

How Bridgepoint Funding Can Help

Bridgepoint Funding is a mortgage broker located in the San Francisco Bay Area. We work with home buyers and homeowners all across the state of California and offer a broad range of loan options.

We can support and facilitate the appraisal process in the following ways:

- Ordering the appraisal as soon as you have an accepted offer, to avoid delays.

- Choosing reliable appraisers who can quickly determine the value of a property.

- Following up to ensure the appraisal is scheduled and the report is on track.

- Reviewing the report for potential issues or discrepancies that might cause delays.

- Helping you understand your options if the appraisal comes in lower than expected.

- Working with you every step of the way for a smooth process and timely closing.

Mortgage questions? If you have questions about using a mortgage loan to buy a house in California, including the various costs that are involved, please contact our staff.