Jumbo loans are a popular mortgage option among home buyers in California, due to the…

Determining the Maximum VA Loan Amount in California

We’ve covered a lot of VA loan-related topics on our blog. But there’s one topic in particular that seems to generate the most interest among borrowers. A lot of people want to know about the maximum VA loan amount here in California.

The short version: The VA used to have official loan limits for all borrowers. But they changed that rule in 2020. Today, most home buyers in California do not have an official (government-imposed) borrowing limit. It’s up to the lender to decide. We have closed VA loans in amounts well over $1 million.

How the VA Loan Program Works

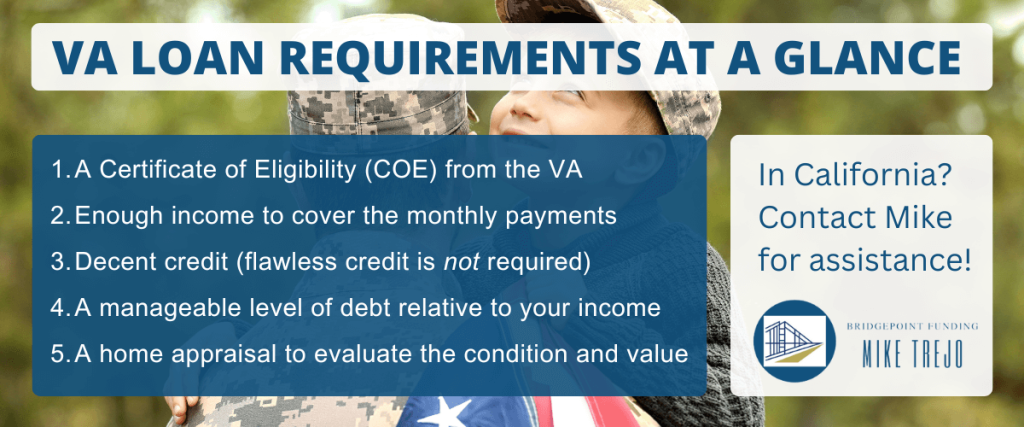

The Department of Veterans Affairs does not lend money directly to borrowers. This is a common misconception among borrowers, so let’s clear it up right away.

The VA guarantees loans that are originated by mortgage lenders in the private sector. You get the money to buy a home from a lender, and the lender gets some degree of protection from the federal government (through the VA).

This insurance is designed to protect lenders from losses that could result from borrower default. Because of this government backing, eligible borrowers can buy a home with no down payment whatsoever, and also without mortgage insurance.

VA loan benefits for California home buyers include:

- No down payment is required for most borrowers. This could reduce your upfront out-of-pocket expense by tens of thousands of dollars, depending on the home price.

- VA loans offer lower interest rates than conventional, on average.

- No private mortgage insurance (PMI), which is typically required for conventional loans with low down payments.

- The VA loan is a lifetime benefit that can be used multiple times over the years.

- You could refinance into a lower interest rate down the road, with less hassle than traditional refinancing.

Most Borrowers Do Not Have an Official Loan Limit

Most home buyers in California who use VA loans do not have a government-imposed size limit. This means you can borrow the maximum amount allowed by your mortgage lender.

Your lender will review your current income and financial situation, including all existing debts, to determine how much you can borrow with a VA loan.

That’s for borrowers with full entitlement in the program.

But those borrowers with “remaining entitlement” might still have an official VA-imposed loan limit. Whether or not you have such a limit will depend on which group you fall into:

Group 1: Full Entitlement / No Loan Limit

If you have full entitlement, there is no VA-imposed limit on the amount you can borrow. You could buy a home in California with no down payment, and it’s up to your mortgage lender to decide the maximum amount.

You have full entitlement if any of the following apply:

- You’ve never used your VA home loan benefit in the past.

- You’ve paid off a previous VA loan and sold the property, restoring your full entitlement.

- You had a foreclosure or short sale on a previous VA loan but have fully repaid the VA.

Group 2: Remaining Entitlement / Loan Limits Apply

If you have remaining entitlement (a.k.a., reduced entitlement), you do have an official VA-imposed loan limit. If you need to borrow more than the official limit for your county, you’ll probably need to make a down payment based on the difference.

You have remaining entitlement if any of the following apply:

- You have an active VA loan you’re still paying back.

- You’ve paid off a previous VA loan but still own the home.

- You’ve refinanced a VA loan into a non-VA loan and still own the home.

- You had a short sale, foreclosure, or deed in lieu of foreclosure on a previous VA loan and haven’t fully repaid the VA.

In cases where there is remaining or reduced entitlement, the VA uses the conforming loan limits established by the Federal Housing Finance Agency (FHFA). These limits vary by county because they are based on median home prices.

As it states on the VA.gov website: “if you’re able and willing to make a down payment, you may be able to borrow more than the county loan limit with a VA-backed loan. Remember, your lender will still need to approve you…”

California VA Mortgages Over $1 Million

To recap: If you’ve never used a VA loan before, or if you used one but paid it off when selling the home, you should have full entitlement in the program. In that case, you don’t have an official loan limit or maximum mortgage amount and can borrow as much as your lender will allow.

As a mortgage broker in the San Francisco Bay Area, we often work with borrowers who use VA loans that exceed $1 million. This is a common occurrence, because the median home value in the Bay Area is well over $1 million.

As a borrower, you should know that it’s possible to borrow well over $1 million with a VA-backed mortgage loan, as long as you have the income to support it.

DTI Ratios and Compensating Factors

When you apply for a VA loan in California, your lender will review your current financial situation to determine how much you can borrow.

This is true for both full entitlement and reduced entitlement scenarios.

Mortgage lenders use the debt-to-income ratio and other metrics to determine the maximum VA loan amount for borrowers.

The debt-to-income (DTI) ratio shows how much of your gross monthly income goes toward your recurring monthly debts. For example, a person with a DTI ratio of 30% uses 30% of their income to cover their debts each month.

The Department of Veterans Affairs states that “the acceptable debt-to-income ratio for a VA loan is 41%.” But they go on to explain that there are numerous exceptions to this general rule.

If the mortgage underwriter can identify certain compensating factors, a borrower with a DTI above 41% could still qualify for a VA loan. In fact, the debt ratio could be as high as 50% if compensating factors are documented:

Compensating factors for VA loans include, but are not limited to, the following:

- Excellent credit history

- Conservative use of credit

- Relatively low level of debt

- Long-term employment

- Significant liquid assets (cash, savings, money market)

- Sizable down payment (even when it’s not required)

- Little or no increase in housing expense

- Satisfactory homeownership experience

- High residual income

As you can see, the VA loan program has a lot of flexibility built into it. The Department of Veterans Affairs gives mortgage lenders plenty of leeway to make prudent lending decisions. Compensating factors are just one example of this.

It Comes Down to Your Ability to Repay

Like other government-backed mortgage programs, VA loans have specific rules and requirement. Some of those rules can affect the maximum amount you’re able to borrow toward a home purchase.

But these guidelines exist for a reason. They are designed to prevent borrowers from taking on too much debt with the addition of a mortgage loan, which could result in financial hardship.

Ultimately, it all comes down to your ability to repay the loan. Lenders use credit scores, debt ratios, income verification, and other tools to ensure that each borrower has the capacity to repay the debt.

Need a VA Loan in California?

At Bridgepoint Funding, we are passionate about this home loan program because it rewards our brave service men and women. In fact, we specialize in providing VA-backed mortgages for California home buyers and homeowners. And we’ve been doing it for nearly 20 years.

If you have questions about the program, or would like to determine the maximum amount you can borrow, please contact our staff for assistance!