This article is part of an ongoing series that answers common questions about different types…

Is It Easy or Hard to Qualify for a VA Loan in California?

California military members and veterans tend to have a lot of questions about the VA home loan program. One of the most common questions has to do with the program requirements and the overall qualification process.

A lot of people want to know: “Is it easy or hard to qualify for a VA loan in California?”

The short answer: This is actually one of the easiest mortgage programs to qualify for, as long as you meet the basic requirements regarding military service and income.

These loans are partially guaranteed by the federal government, via the U.S. Department of Veterans Affairs. Because of this, mortgage lenders can be more lenient with regard to qualification criteria.

VA Loans: One of the Easiest Mortgages to Obtain

In order to understand the mortgage loan qualification process, you first have to understand how the program works.

VA loans are one example of a government-backed mortgage. Federal Housing Administration (FHA) loans are another example. In both cases, the federal government insures or guarantees the loan to protect the lender from potential financial losses related to borrower default.

This added “layer” of protection enables lenders to be a bit more flexible when it comes to credit scores, debt ratios, and other mortgage qualifications.

This government backing also makes it fairly easy to qualify for a VA loan in California, as long as you meet the military service standards. You don’t even need a down payment or perfect credit, as we’ll discuss below.

In California, the following groups are typically eligible for VA home loans:

- Active-duty military who have served for at least 90 days continuously

- National Guard and Reserve members who have completed at least six years of regular service or 90 days of active duty

- Veterans who were discharged for a service-connected disability, even if they served less than 90 days on active duty

- Surviving spouse of a service member who died in the service or due to a service-related disability

Minimum Qualification Requirements

As mentioned above, it’s fairly easy to qualify for a VA-guaranteed mortgage loan in California, as long as you meet a few basic requirements.

The most important thing is that you have sufficient income to manage your monthly payments and repay your loan over time. To verify this, lenders will examine your pay stubs, bank statements, and tax records.

As for credit scores, the VA does not impose any minimum score requirement. They leave that up to the lender to decide.

In some cases, it’s possible to qualify for a VA loan in California with a credit score down into the 500 range. Conventional mortgage programs, on the other hand, typically require a score of 600 or higher and can be stricter in other areas as well.

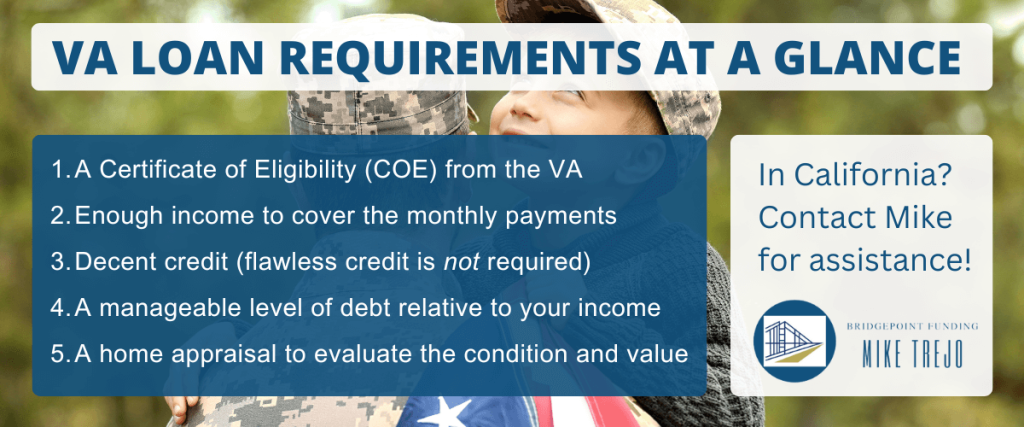

Here are some things you’ll need to qualify for a VA home loan:

- A Certificate of Eligibility (COE) from the Department of Veterans Affairs

- A decent credit score, but it doesn’t have to be perfect

- A manageable level of debt with the addition of the mortgage loan

- Enough income to cover your monthly loan payments and other debts

- A home in good shape without any major structural or health hazards

Bottom line: VA loans have some of the most relaxed and lenient requirements in the mortgage world, making them easier to obtain than other loan types.

How This Program Benefits Home Buyers

We’ve covered one important benefit of using a VA loan to buy a house in California. It’s often the easiest type of mortgage loan to qualify for, due to the government backing described above.

But this program offers other advantages as well, from a home buyer’s perspective:

1. No down payment required.

This is the biggest benefit of using a VA loan when purchasing a house. Eligible borrowers who use this program can buy a home with no down payment whatsoever. This reduces the amount of money you have to save, and allows you to purchase a property sooner.

The VA loan program is one of the few mortgage options that offer 100% financing. And in a pricey real estate market like California, that’s a pretty big deal.

2. No mortgage insurance.

Typically, when a borrower takes on a mortgage loan that covers most or all of the purchase price, mortgage insurance will be required. This increases the size of the borrower’s monthly payments, as well as the total amount of money paid over time.

But mortgage insurance is usually not required for VA loans in California. This is a key money-saving benefit for military members, veterans, and their families.

3. Limit on closing costs.

The Department of Veterans Affairs limits the amount of fees lenders can charge borrowers who use VA home loans. This is another money-saving feature that benefits you, as the borrower.

Additionally, the department allows sellers to contribute money toward the buyer’s closing costs. This gives you more flexibility when negotiating the terms of the sale, and could further reduce your out-of-pocket expense.

4. Competitive mortgage rates.

California VA loans are backed by the federal government. Because of this, lenders are often willing to offer lower rates for VA loans, compared to conventional mortgage products.

Of course, the rate you receive will partly depend on your credit score and other factors. But in general, VA borrowers commonly end up with great rates. A lower rate reduces your total borrowing costs.

5. Flexible credit standards.

Because of the government backing associated with this program, VA loans offer some of the most flexible underwriting guidelines. This means you don’t need perfect credit to qualify for financing. The debt-to-income ratio guidelines tend to be more flexible as well.

Overview of the Application and Approval Process

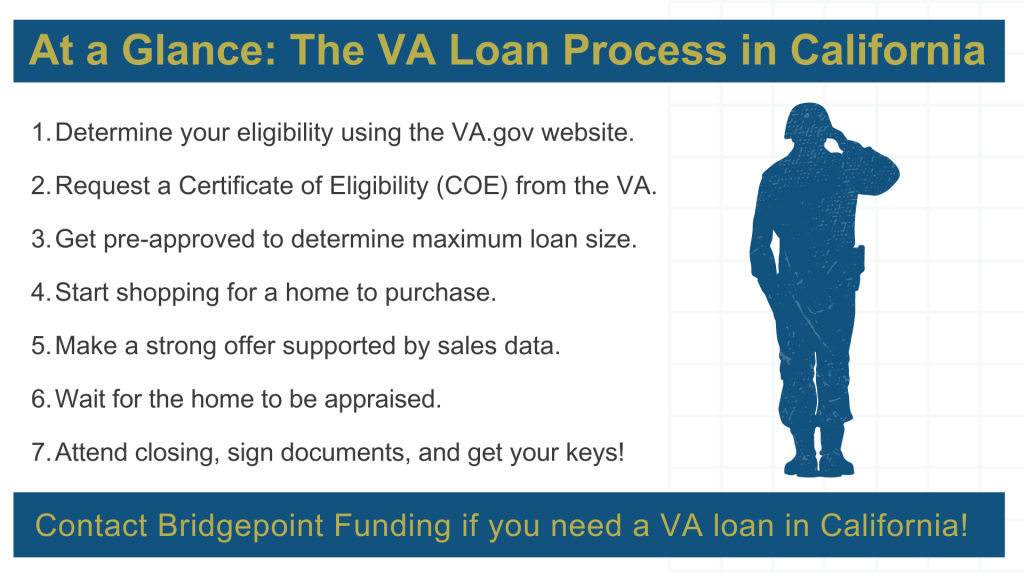

The VA loan application process is fairly easy to navigate as well, once you have a few documents. The first step is to obtain your Certificate of Eligibility (COE).

The COE is a document issued by the U.S. Department of Veterans Affairs (VA) that verifies your eligibility for this program. You can request this documefnt through the VA.gov website, or have the mortgage lender do it for you.

Note: If you’re buying a home in California, we can assist you with this process. We specialize in the VA loan program and serve borrowers all across the Golden State.

You will need to provide some other standard documentation as well, like any other type of mortgage loan. This includes some of the items mentioned earlier – pay stubs, bank statements, tax records, and a “gift letter” if someone else is contributing money to your down payment.

After that, the process moves forward as it would with a regular mortgage:

- You can get pre-approved for a specific loan amount.

- You’ll shop for a home and submit an offer.

- The home will be appraised to determine its market value and condition.

- The loan and the property will be underwritten to make sure everything checks out.

- You’ll eventually attend the closing, sign all finalized documents, and collect your keys.

Please contact us if you have questions about this program or would like to apply. We serve borrowers all across the state of California.