As a home buyer in California, you have many different options when it comes to…

California FHA Mortgage Insurance: Upfront and Annual MIPs Explained

Home buyers in California who use an FHA loan to buy a house typically have to pay for mortgage insurance. That’s one of the requirements set forth by the Federal Housing Administration and HUD.

This guide explains what FHA mortgage insurance is, how it works, and why it’s required.

Here are five things you should know right off the bat:

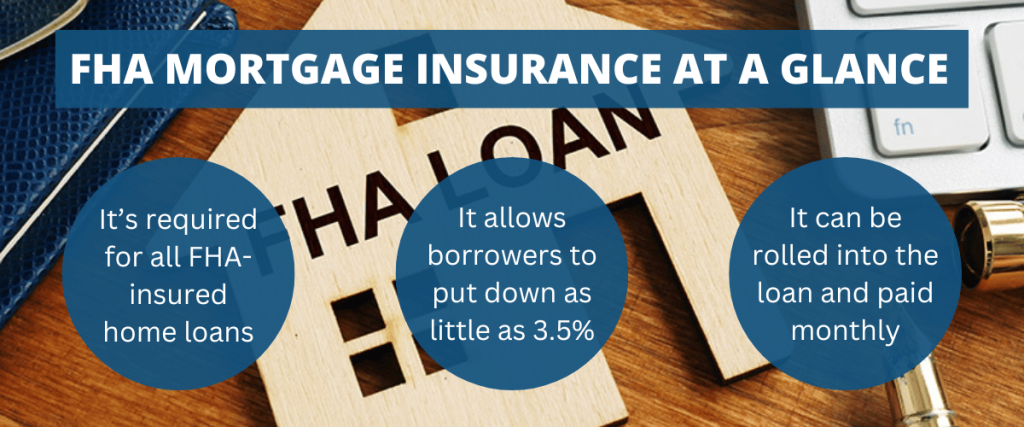

- All California home buyers who use FHA loans have to pay for mortgage insurance.

- This insurance protects lenders from financial losses relating to borrower default.

- It benefits borrowers by offering small down payments and flexible credit criteria.

- FHA loans require an upfront and annual premium. Both can be rolled into the loan.

- Most borrowers have to pay this insurance for as long as they keep the home loan.

How FHA Mortgage Insurance Works

FHA loans are similar to other types of mortgage loans, but with one key exception. They are insured by the government, through the Federal Housing Administration.

This insurance protects participating mortgage lenders from losses that occur when a borrower defaults (or fails to repay) the mortgage debt.

Contrary to popular belief, FHA mortgage insurance is not designed to protect the borrower. But it benefits the borrower by allowing mortgage lenders to offer low down payments and flexible credit requirements.

In California, FHA loans are generally easier to obtain than regular/conventional mortgage loans. The government-provided insurance makes that possible.

Key point: While home buyers do not receive protection from FHA mortgage insurance, they do have to pay for it. So let’s shift gears and talk about the cost of these premiums.

Cost Breakdown: Annual vs. Upfront MIP

As mentioned above, the FHA loan program requires California home buyers to pay a mortgage insurance premium (MIP) on their loans. These premiums help fund the program and are therefore an essential component that keeps it operating.

There are actually two kinds of FHA mortgage insurance for California home buyers who use this program, and the overall cost can vary:

- Upfront: There is an upfront premium that typically equals 1.75% of the loan amount. It’s a one-time cost. Borrowers can either pay it upfront, as the name suggests, or roll it into the loan.

- Annual: There’s also an annual mortgage insurance premium. The cost can vary depending on the loan size and term. For most borrowers who use this program, the annual insurance premium equals 0.55% of the loan amount per year (divided into 12 monthly installments).

This is a source of confusion for a lot of home buyers. So let’s take a closer look at both the upfront and annual FHA mortgage insurance premiums required in California.

Part 1: The Upfront Insurance Premium

The upfront mortgage insurance premium (UFMIP) for FHA loans typically comes out to 1.75% of the loan amount, or 175 basis points. It’s a one-time charge, not a recurring expense.

According to HUD Handbook 4000.1, the official policy guide for this program:

“The UFMIP charged for all amortization terms is 175 Basis Points (bps), unless otherwise stated in the applicable Programs and Products or in the MIP chart.”

The “amortization terms” part of that quote refers to the length of the loan. Whether you’re using a 15-year or a 30-year FHA loan in California, the upfront mortgage insurance premium is the same.

So, if you use an FHA loan to buy a home in California, an upfront mortgage insurance premium will be applied. In that scenario, you can expect to pay 1.75% of the loan amount.

Despite the “upfront” name, this fee can be rolled into the mortgage and paid over time. Financing it will increase the size of your monthly payments, but only by a modest amount.

Part 2: The Annual Insurance Premium

In addition to the upfront MIP, home buyers who use FHA loans also have to pay an annual mortgage insurance premium — sometimes for the life of the loan.

In California, the annual mortgage insurance can vary depending on the amount of money being borrowed and the loan length or “term.” The annual premium usually gets added onto the monthly payments, on top of the monthly principal and interest.

Most home buyers who use an FHA loan make a down payment below 5%, which requires an annual mortgage insurance premium of 0.55%.

Example: A person borrowing $600,000 with an annual mortgage insurance premium of 0.55% would pay $3,300 per year for MIP (or approximately $729 per month).

For most borrowers in California, FHA mortgage insurance is required for the life of the loan. But there are some scenarios where it might only be applied for 11 years.

Here are the general rules and guidelines regarding cancellation:

- If your initial loan-to-value (LTV) ratio is 90% or less, you will pay the annual MIP for at least 11 years. After that, you may be eligible to cancel the MIP.

- If your initial LTV ratio is more than 90%, you will probably have to pay the annual MIP for the entire duration of the loan.

As you can see, the annual premium is a lot more confusing when compared to the upfront premium, which is a one-time flat fee.

How It Differs From Conventional PMI

This would be a good place to clarify the difference between FHA and conventional loans.

- FHA loans are insured by the Federal Housing Administration, as described earlier.

- Conventional loans do not receive any kind of government insurance backing.

Mortgage insurance can be required for both FHA and conventional loans. The difference is that it’s almost always required on the FHA side, while home buyers who use conventional loans can avoid mortgage insurance by making a down payment above a certain amount.

Unlike an FHA loan, which requires mortgage insurance for all borrowers, conventional home loans only require it in certain situations. PMI is usually required when a borrower makes a smaller down payment that results in a loan-to-value (LTV) ratio above 80%.

So, the best way to avoid mortgage insurance entirely is to use a conventional loan with a down payment of at least 20%. Borrowers can also use a “piggyback” strategy to avoid PMI.

But with an FHA loan, insurance is always required, regardless of how much you put down.

How It Benefits Home Buyers in California

Some home buyers in California find FHA mortgage insurance confusing due to the fact that it protects the lender while the borrower pays for it.

Why should a borrower pay for coverage that protects someone else?

The truth is that home buyers can directly benefit from this mortgage insurance program, even though it’s designed to protect the lender.

By providing protection for lenders, FHA loans make homeownership more attainable for a much larger pool of home buyers.

Here’s how the HUD.gov website explains it:

“FHA mortgage insurance protects lenders against losses. If a property owner defaults on their mortgage, we’ll pay a claim to the lender for the unpaid principal balance. Because lenders take on less risk, they are able to offer more mortgages to homebuyers.”

Without mortgage insurance, most home buyers would have to make a down payment of 20% or more. They would also need excellent credit scores with few or no credit-related issues in the past.

With mortgage insurance, home buyers in California can qualify for financing with less money down and more flexible credit criteria. It helps clear a path to homeownership.

In short: The FHA loan program benefits home buyers who might not qualify for a regular home loan due to their credit score and/or lack of down payment funds.

So, while these premiums can slightly increase the size of your monthly payments, the benefits tend to outweigh the cost. That’s why millions of home buyers use FHA-backed mortgages each and every year.

Key Points to Take Away From This Guide

We’ve covered a lot of important (and sometimes confusing) information in this guide. Here are the most important things you should take away from it.

- FHA loans are insured by the Federal Housing Administration to protect lenders from borrower defaults. This insurance enables lenders to offer lower down payments and more flexible credit requirements.

- FHA mortgage insurance protects the lender, not the borrower. However, borrowers must pay for it, typically through two types of premiums: upfront and annual.

- Borrowers pay a one-time upfront fee equal to 1.75% of the loan amount. This can be paid at closing or rolled into the loan, increasing monthly payments slightly.

- Borrowers also pay an annual premium (commonly 0.55% of the loan amount). This cost is added to monthly payments and may last for the life of the loan unless certain criteria are met (e.g., low initial loan-to-value ratio).

- FHA loans always require mortgage insurance, regardless of the down payment size. In contrast, conventional loans only require private mortgage insurance (PMI) when the loan-to-value ratio exceeds 80%.

- While the insurance protects lenders, it makes homeownership more accessible for borrowers with limited savings or lower credit scores. This flexibility benefits first-time buyers or those who might not qualify for conventional loans.

Have questions? We offer both FHA and conventional loans and serve borrowers all across California. Please contact our staff if you have mortgage questions or wish to apply for a loan.