When buying a home in California, or even when simply researching the process, you'll eventually…

Closing Costs vs. Down Payments When Buying a House in California

Home buyers in California tend to have a lot of questions about closing costs and down payments. And rightfully so. When combined, these upfront expenses can amount to tens of thousands of dollars.

So you need to understand what they are and how they work.

In this guide: You’ll learn about the relationship between closing costs and down payments in California, and what you can do to overcome these upfront hurdles.

Similarities and Differences

When it comes to buying a home in California, there are similarities and differences between closing costs and down payments. The first thing to know is that they are not the same thing. In fact, they aren’t directly connected in any way.

- Down Payment: This is the amount of money a buyer pays upfront when purchasing a home. It’s typically expressed as a percentage of the home’s purchase price. The down payment is used to reduce the amount of the loan needed from the mortgage lender.

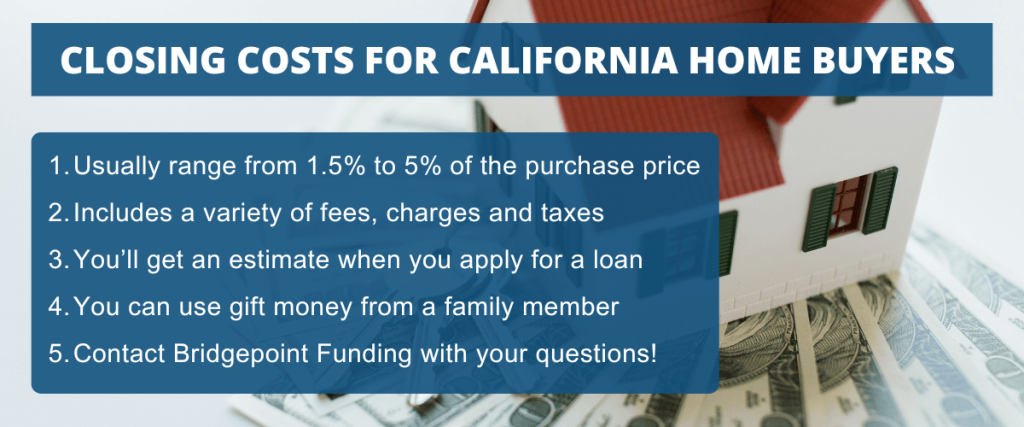

- Closing Costs: These are fees and expenses that home buyers must pay at the end of the real estate transaction. Closing costs can include loan origination fees, title insurance, appraisals, attorney fees, and more. They usually range from 1.5% to 5% of the home’s purchase price and are paid in addition to the down payment.

What closing costs and down payments have in common is the fact that you have to pay them upfront, in order to close the transaction. This means home buyers have to save enough money to cover both of these expenses, in order to qualify for a mortgage loan.

Both the down payment and closing costs have to be paid on or before the final closing day. When you “close” on a home, you will finalize and sign all of the documents relating to the property transfer. You’ll also provide a cashier’s check or wire transfer to cover all of your closing costs.

But the similarities end there. Closing costs are a collection of fees and charges that can accumulate during the home buying process. The down payment is an upfront investment that goes toward the sale price.

Main difference: Your down payment is part of the investment you’re making in the house, while the closing costs are more like administrative fees or service charges.

An Explanation of Closing Costs

When you buy a house in California, you will receive professional services from a number of different people and organizations. These can include the following:

- Property tax and recording services from local government offices

- Mortgage origination and processing services from your lender

- Title research services from a title company (to verify ownership rights)

- And possibly legal guidance from a real estate attorney

Collectively, all of these service charges are referred to as your “closing costs.” And on a median-priced home in the state of California, they might range from $10,000 to $30,000 — or even more.

But they are not related to the down payment in any way. They are two separate things. Home buyers in California pay closing costs on top of the down payment, which underscores the importance of saving money early.

Key point: When you apply for a loan, the lender will check to see that you have the funds needed for all of your upfront expenses. They’ll do this by reviewing your bank statements and other financial records.

An Explanation of Down Payments

Let’s shift gears now and talk about the down payment you might encounter when buying a home in California.

Unlike closing costs, which are basically the cost of doing business in the real estate world, the down payment gets applied toward your purchase. That means the money gets invested into the home when you finalize the sale.

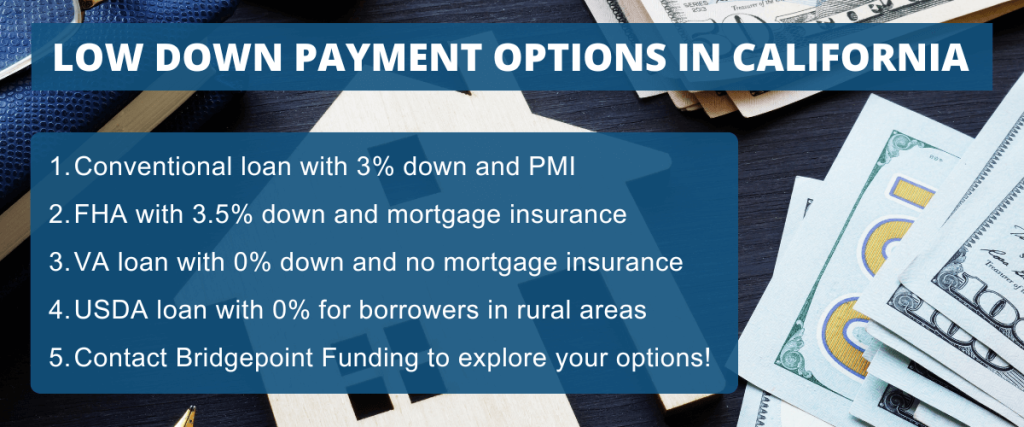

Most home buyers in California have to make a down payment of some kind. The one exception is for military members and veterans who qualify for the VA loan program. VA loans offer 100% financing, which means eligible borrowers can buy a house with no money down.

For a conventional home loan (that’s not insured by the government), a typical down payment can range from 3% to 20% depending on the scenario. The FHA loan program, which is popular among first-time buyers in California, allows borrowers to put down as little as 3.5%.

Myth busting: It’s a misconception that all home buyers have to make a down payment of 20% or more. As mentioned above, some loan programs allow for a down payment as low as 3% to 5%.

The Benefits of Using ‘Gift Money’

The down payment and closing costs on a typical home purchase in California can add up to a significant sum of money. As a result, some home buyers struggle to overcome these upfront hurdles, even though they could comfortably afford the monthly payments.

There’s a solution for this challenge. It’s called gift money.

These days, most mortgage loan programs allow borrowers to use gift money from an approved source. The gifted funds can be put toward the home buyer’s down payment and/or closing costs.

A common example involves parents providing funds to help their (adult) children buy a home in California. This is sometimes referred to as the “Bank of Mom and Dad,” jokingly.

But it’s no joke. This strategy could greatly reduce the amount of money you have to pay out of your own pocket, clearing a path to homeownership. So it’s worth considering at the very least.

Different loan programs have different rules and requirements when it comes to gift money. But they all require a letter from the person providing the funds, stating that they do not expect repayment.

A Good Reason to Start Saving Money Now

If you do the math regarding down payments and closing costs, you’ll see that they can add up to a sizable amount. Even on a moderately priced home (by California standards), these two expenses combined could easily exceed $30,000.

Because of this, it’s wise to start saving money as soon as possible. If you believe that you’ll be buying a home in California in the near future, now is the time to start saving.

The more money you can save between now and the time you enter the market, the better prepared you will be. You’ll also have an easier time qualifying for a mortgage loan, if you have sufficient funds in the bank already.

Nine Key Points to Take Away From This

We’ve covered a lot of information in this guide, and it’s all important. So let’s conclude with a summary of the most important takeaways:

- Closing costs and down payments are significant upfront expenses when buying a home in California.

- The down payment is the upfront investment in a home, expressed as a percentage of the purchase price.

- Closing costs are fees paid at the end of the transaction, to cover services like loan origination, title insurance, and appraisal.

- In a typical real estate transaction, both of these expenses have to be paid at closing.

- Closing costs in California typically range from 1.5% to 5% of the home’s price and are separate from the down payment.

- Down payments can vary, with conventional loans requiring 3% to 20% and FHA-insured home loans allowing for as little as 3.5%.

- Your mortgage lender will verify that you have enough “cash to close” before approving the loan.

- Home buyers in California could also use gift money from an approved donor.

- The sooner you start saving for your down payment and closing costs, the better.

Have mortgage questions? Bridgepoint Funding is here to help. We offer a variety of mortgage options with flexible down payment requirements, and we serve borrowers all across the state of California!