As a home buyer in California, you have many different options when it comes to…

When Is PMI Required in California, and Related FAQs

We’ve covered private mortgage insurance in previous articles, from a cost perspective. To further clarify this subject, we have created a list of frequently asked questions relating to private mortgage insurance in California.

This guide includes one of the most common questions among home buyers: When is PMI required in California?

In short: If you use a conventional mortgage loan that accounts for more than 80% of the home’s value, you’ll probably have to pay PMI. But you can cancel it later on, once you reach a certain equity level.

What is private mortgage insurance?

Private mortgage insurance (PMI) is a type of insurance that protects the lender in case a borrower defaults on their mortgage loan. A “default” occurs when a homeowner with a mortgage is no longer able to make their monthly payments.

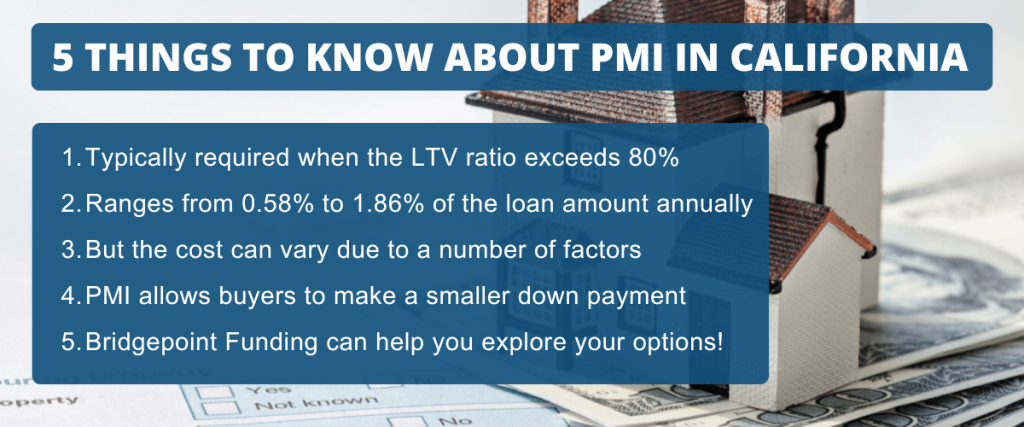

In California, PMI is usually required when a home buyer takes out a loan that accounts for more than 80% of the property’s value. In other words, when the loan-to-value (LTV) ratio rises above 80%, PMI coverage is typically required.

Private mortgage insurance is unique in the sense that it protects the bank or lender rather than the borrower, though the borrower is the one who pays for it.

But a bit later, you’ll understand how PMI benefits the home buyer as well.

When is PMI required in California?

In California, lenders usually require PMI when a home buyer makes a down payment of less than 20%, resulting in an LTV ratio above 80%.

The loan-to-value (LTV) ratio compares the dollar amount of a loan to the appraised value of the home being financed. It’s calculated by dividing the loan amount by the asset’s value, then expressing the result as a percentage.

Example: If a person borrows $400,000 to purchase a home valued at $450,000, the resulting LTV ratio would be 88.9% and would likely require PMI.

Lenders consider a lower down payment to be a higher risk, because it requires them to put more money into the property. Private mortgage insurance helps mitigate that risk and gives lenders the confidence to offer loans with smaller down payments.

Once the homeowner builds equity in the property and reaches a loan-to-value (LTV) ratio of 80% or less, they should be able to cancel PMI.

How does PMI work?

When a borrower in California obtains a mortgage with PMI, they pay a monthly premium as part of their overall mortgage payment. The exact premium amount is based on the loan amount, the LTV ratio, and the borrower’s credit score.

The monthly PMI payments are usually put aside in an insurance pool. If a borrower defaults (or stops paying) on the mortgage, the lender can use the funds from the insurance pool to recover some of their losses.

How does it benefit the home buyer?

While private mortgage insurance in California is designed to protect the lender, it offers some important advantages to home buyers as well. For one thing, PMI enables home buyers to qualify for a mortgage with a much smaller down payment.

By allowing borrowers to make a down payment of less than 20%, PMI helps reduce the upfront cash required to purchase a home. This in turn makes homeownership more accessible to those who haven’t yet saved a substantial down payment.

When this guide was last updated, the median home price in California was around $773,000. With that number in mind, consider the following scenarios:

- 20% down payment to avoid PMI = $154,600

- 3% down payment with PMI = $23,190

As you can see, taking on private mortgage insurance allows borrowers to buy a home sooner rather than later, by greatly reducing the upfront investment.

How much does PMI cost in California?

The cost of PMI can vary depending on several factors, including the size of the down payment, the loan amount, the borrower’s credit score, and the specific terms offered by the lender.

The premiums typically range from 0.58% to 1.86% of the original loan amount per year. This amount is divided into monthly premiums and added to the borrower’s mortgage payment.

For example, if a borrower in California took out a $500,000 mortgage loan with a PMI rate of 1%, they could expect to pay around $416 per month for PMI. (The math: 5,000 ÷ 12 = 416)

How long do I have to pay the premiums?

The duration of PMI payments depends on the loan agreement and the progress made in building equity in the property. In many cases, once the homeowner’s loan-to-value (LTV) ratio reaches 80% or less, they can request cancellation of their PMI policy.

Even if you don’t request cancellation when you reach 20% equity, it should happen eventually. The loan servicer is required to automatically terminate PMI when your principal balance is scheduled to reach 78% of the original value of your home.

Can I avoid paying it altogether?

There are basically two ways to avoid PMI in California, when using a mortgage loan:

1. Make a down payment of 20% or more.

This is the simplest and most effective way to avoid private mortgage insurance. When you make a down payment of 20% or more, your loan-to-value (LTV) ratio will be at or below 80%. This reduces the risk associated with the loan and avoids the need for PMI.

2. Combine two loans in a “piggyback” fashion.

If you can’t afford a 20% down payment, you could avoid paying PMI in California by combining two mortgage loans in a “piggyback” strategy.

For example, you could take out a first loan for 80% of the purchase price, along with a second one for 10% – 15% of the price. You would then pay the remaining amount (5% – 10% in this case) out of pocket, in the form of a down payment.

Neither loan would have an LTV over 80%, so private mortgage insurance would not be required.

How can California homeowners cancel PMI?

As mentioned previously, homeowners in California can remove PMI from their mortgages when the loan-to-value ratio drops to 80%. This happens naturally over time, as the homeowner makes regular mortgage payments and reduces the principal balance.

Once this threshold is met, the homeowner can request PMI removal from their lender or servicer.

Another option, at least in some cases, is to refinance the mortgage down the road. Refinancing is when you take out a new home loan that replaces the existing one.

Whether you’ll need to pay for PMI on the new loan will depend on your home’s current value and the principal balance of the new mortgage.

Related article: PMI cancellation in California

Does it protect the borrower or the lender?

Private mortgage insurance policies protect the lender that originates the loan, not the borrower. Its primary purpose is to provide financial protection to the lender in case the borrower defaults on the mortgage loan.

If the borrower stops making mortgage payments and possibly goes into foreclosure, PMI can help the lender recover some of their losses by paying a portion of the outstanding loan balance.

Is it required for government mortgages too?

In California, private mortgage insurance specifically applies to conventional loans where the LTV is more than 80%. The term “conventional” refers to home loans that do not receive government backing, which distinguishes them from programs like FHA and VA.

Federal Housing Administration (FHA) loans have their own version of mortgage insurance. It’s provided through the government instead of a private company. FHA mortgage insurance premiums work similarly to PMI, but they’re required for all FHA loans regardless of the down payment amount.

The VA home loan program, which is available to military members and veterans in California, does not require mortgage insurance at all.

Need help? If you’re in California and have mortgage or PMI-related questions, please contact our staff. Bridgepoint Funding is based in the Bay Area but serves borrowers all across the Golden State.