As a home buyer in California, you have many different options when it comes to…

Scenarios When Mortgage Insurance Is Not Required in California

Mortgage insurance is a common source of confusion for home buyers in California. First-time buyers, in particular, tend to have a lot of questions about how mortgage insurance works, when it’s required, and when it’s not.

In this article, we will explore some of the scenarios where mortgage insurance is not required in California.

Here are the seven most important points covered in this guide:

- Mortgage insurance protects the lender from losses, but the buyer pays for it.

- There are two main types of mortgage insurance in California: government and private.

- Private mortgage insurance is usually required when a person makes a small down payment.

- It’s not required for conventional loans with a loan-to-value ratio of 80% or lower.

- Mortgage insurance is also not required for VA loans used by military members and vets.

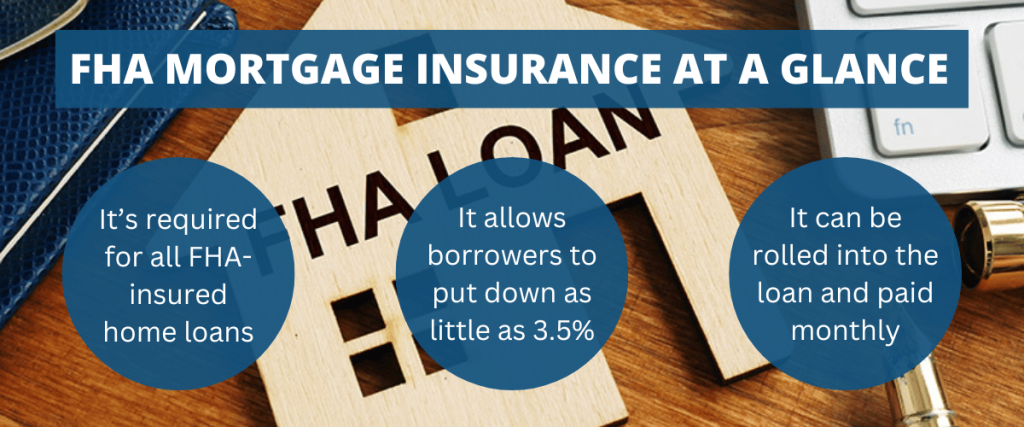

- FHA loans require mortgage insurance for all borrowers, regardless of down payment size.

- Private mortgage insurance (PMI) can be cancelled, while the FHA variety often cannot.

What Is Mortgage Insurance, Exactly?

Mortgage insurance is a financial safeguard that lenders often require when borrowers obtain a home loan with a low down payment. This applies to both conventional and FHA loans.

Mortgage insurance protects the lender in case the borrower defaults on the home loan. It reduces the lender’s risk by ensuring they will recoup their losses if the borrower fails to make their mortgage payments.

Key point: There are two main types of mortgage insurance that are commonly used in the state of California, depending on the type of loan being used: private and FHA.

- Private: Conventional loans, which are not insured or backed by the government, sometimes require private mortgage insurance (PMI).

- Government: FHA loans, which receive government insurance backing, almost always require government-provided mortgage insurance premiums (MIPs).

Let’s take a closer look at these two variations. After that, we’ll explore some of the scenarios when mortgage insurance is not required in California.

1. Private Mortgage Insurance (PMI)

PMI is often required for conventional loans when the loan-to-value (LTV) ratio rises above 80%.

That’s why borrowers often have to pay PMI when making a down payment below 20%. In this scenario, the LTV ratio would be above 80% and would therefore trigger the PMI requirement.

Definition: A conventional loan is one that’s not backed by the government. The “conventional” label distinguishes these regular home loans from government-backed mortgage programs like FHA and VA.

PMI is provided by private insurance companies and paid for by the borrower as part of their monthly mortgage payment. PMI premiums can vary depending on factors like the loan amount, credit score, and down payment size.

The annual premium amount for a California PMI policy is typically expressed as a percentage of the loan amount. According to data from the Urban Institute’s Housing Finance Policy Center, the cost ranges from 0.58% to 1.86% of the loan amount per year, on average.

Borrowers can request the removal of PMI once they reach a specified level of equity in their home, usually 20%. This is a key difference between PMI and FHA mortgage insurance, which we will cover next.

2. FHA Mortgage Insurance Premiums (MIPs)

FHA loans are an example of a government-backed mortgage loan. They’re offered by lenders in the private sector, as with most other types of loans. But they also receive federal insurance backing through the FHA, an agency that’s part of HUD.

FHA loans are popular among first-time home buyers in California, as well as borrowers with lower credit scores. Though they’re not limited to those groups.

FHA mortgage insurance comes in two forms:

- There’s a one-time upfront premium that can be paid at closing or rolled into the loan.

- There’s also a recurring annual premium that’s part of the monthly mortgage payments.

Most home buyers in California who use FHA loans to buy a house have to pay the annual premium for as long as they keep the loan. However, those who make a down payment of 10% or more can cancel their insurance after 11 years.

The takeaway: In both of these scenarios (FHA and conventional), mortgage insurance protects the lender. But it also benefits home buyers by enabling them to buy a home sooner, by putting less money down.

Four Scenarios Where It’s Not Needed

Mortgage insurance is not always required. That’s one of the most important points to take away from all of this.

Many home buyers in California who use mortgage loans to facilitate their purchases are able to avoid paying mortgage insurance altogether. This in turn reduces the size of their monthly payments.

Here are four scenarios where mortgage insurance is not required in California:

1. Making a down payment of 20% or more

If the borrower can make a down payment of at least 20% on a conventional loan, they can often avoid the need for mortgage insurance. This is because a 20% down payment is considered a strong indicator of financial stability and lowers the lender’s risk. It also keeps the loan-to-value ratio at or below 80%, avoiding the PMI requirement.

2. Using the VA loan program

Many military members and veterans in California are eligible for VA loans, which are guaranteed by the U.S. Department of Veterans Affairs. These loans do not require mortgage insurance, regardless of the down payment amount.

The VA loan program also allows eligible borrowers to buy a house with no down payment whatsoever. This makes it one of the best financing options for military members and veterans.

3. Using a USDA “rural” home loan

The U.S. Department of Agriculture (USDA) offers loans for rural home buyers who meet certain income requirements. They’re commonly known as “USDA loans.” These loans also do not require mortgage insurance, making them an attractive option for eligible borrowers.

California home buyers who use USDA loans do have to pay an “annual guarantee fee.” But this fee usually costs a lot less than the private mortgage insurance assigned to conventional loans.

As it states on the USDA.gov website:

“USDA Rural Development (RD) Single-Family Housing Direct loans have no private mortgage insurance. USDA Guaranteed Loans are charged an annual guarantee fee instead of mortgage insurance. Guarantee fees are paid to USDA by the approved lender and are usually included in the homeowner’s monthly loan payment.”

In most cases, the USDA annual fee amounts to 0.35% of the outstanding mortgage balance, divided into 12 monthly payments.

4. Combining two mortgage loans in a “piggyback” fashion

Some borrowers choose to combine a first mortgage and a second mortgage (known as a piggyback loan) to avoid paying mortgage insurance.

For example, a home buyer could make a 10% down payment, take out an 80% first mortgage, and a 10% second mortgage, effectively avoiding mortgage insurance. In this scenario, neither of the two loans would have an LTV above 80%. So mortgage insurance would not be required.

Mortgage questions? Bridgepoint Funding offers a wide range of mortgage options and serves borrowers all across the state of California. Please contact us if you have questions about financing your home.