In the San Francisco Bay Area, home buyers often find themselves caught up in multiple-offer…

How Long Is the Escrow and Closing Process in California?

“How long is the escrow and closing process in California, and what are the various steps that have to occur before closing?”

These are common questions among California home buyers, especially first-time buyers who are new to the process. So we’ve created an in-depth guide to help you understand how the escrow process usually works.

The Escrow Process Defined

Let’s start with a quick definition. The term “escrow” refers to the time frame and events between contract and closing. It starts when you sign a purchase contract with the seller, and it ends when you close on the house.

That term can also refer to the escrow company that manages the process, and the special escrow account that’s set up to handle the funds.

So the word can have different meanings based on its usage, as in the following sentences:

- “During the escrow period, we had to arrange a home inspection and secure a mortgage.”

- “The escrow process was smooth, and we closed on the house within a month.”

- “Our escrow company handled all the paperwork and communication with the title company.”

- “The buyer’s earnest money deposit will be held in an escrow account until the closing.”

Whether you’re talking about the process, account, or company, the concept is the same. This system helps to ensure that the buyer and seller fulfill their obligations before money or property officially changes hands.

Important Steps Between Contract and Closing

In California, the escrow and closing process can vary from one transaction to the next due to a number of factors. But it usually follows a logical sequence of events that includes the following steps:

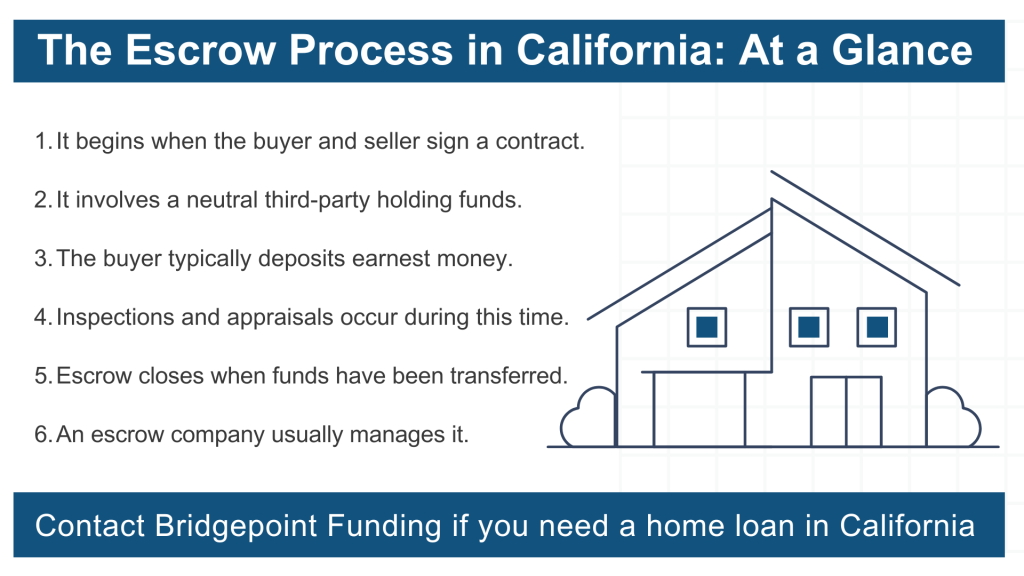

1. The buyer makes an offer to start the escrow process.

The escrow process starts when the home buyer signs a real estate purchase agreement or contract with the seller.

In most cases, the buyer will also make an earnest money deposit at this point. The initial documents and deposit money are eventually delivered to the escrow agent or another neutral third party.

In California, the seller often chooses the escrow company. But that’s not a rule or requirement. The buyer could choose the company as well. It just needs to happen so the deal can move forward, and both sides need to agree.

2. The mortgage lender orders a home appraisal.

Once the buyer and seller have officially “entered escrow,” the mortgage lender will order a home appraisal. The appraiser’s job is to determine how much the house is worth in the current market.

This helps prevent a situation where the home loan exceeds the value of the property. The appraisal is another important step in the California escrow process, so we’ve created a separate in-depth tutorial to help you understand how it works.

3. The title company reviews the title to verify ownership.

In real estate, the “title” is a legal term that refers to property ownership. When you have the title to something, you own it.

As part of the escrow process, a title company will usually check to ensure that there is a clear chain of ownership, with no liens or court filings that might prevent a sale. This protects the home buyer and mortgage lender alike.

4. The escrow company will gather documents.

The mortgage lender produces a variety of documents relating to the home loan and delivers them to the escrow agent or company. The escrow agent will check these “loan docs” and other paperwork to ensure that everything is complete and ready for closing.

5. The buyer attends closing and signs all finalized documents.

This is the final step in the California escrow process, and arguably the most important. At this stage, the home buyer will provide a check or wire transfer to cover their closing costs and down payment. The buyers and sellers will also sign a variety of documents relating to the sale.

The title or escrow company will update the status of the title to reflect the transfer of ownership. Mortgage documents will be returned to the lender after they’ve been signed. Shortly after that the lender will release the funds.

How Long Does it Take to Close in California?

In California, as in many states, the real estate escrow process can take around 30 to 40 days on average. That’s from the time the seller accepts the buyer’s offer, all the way through to the day of closing.

It can go longer in the case of a more complicated transaction. It can also happen faster if everything goes smoothly and there are no backlogs.

Some homes clear the title search process without any issues. Other properties might have title “defects” (such as a lien or legal judgment) that require additional research. Additionally, a backlog at the escrow company could affect the timeline.

In most cases, however, escrow can be closed successfully within the agreed-upon timeframe. It’s only in rare circumstances that things get delayed to the point of rescheduling the closing.

As a home buyer, the best thing you can do during the escrow process is to stay in close contact with your mortgage company. If they need any additional information, deliver it as quickly as possible. This will help keep the closing on track — which is what everyone wants.

Glossary of Important Escrow Terms

The glossary below includes some of the most important terms that relate to the escrow process in California. Home buyers should at least have a basic understanding of what these terms mean.

Closing: The final stage of a real estate transaction where ownership of the property is transferred from the seller to the buyer.

Closing Costs: Expenses beyond the purchase price of a home that buyers and sellers must pay to complete a real estate transaction. These costs typically include loan fees, title insurance, escrow fees, and property taxes.

Contingency: A condition written into a real estate contract that must be fulfilled before the transaction can proceed. Common contingencies include home inspections, financing approval, and appraisals.

Deed: A legal document that transfers ownership of real property from one party to another. The deed is usually signed at closing.

Earnest Money: A good-faith deposit made by the buyer at the beginning of the escrow process to show their commitment to purchasing the home. This amount is typically applied toward the down payment or closing costs.

Escrow: A neutral third party that holds funds and documents related to a real estate transaction until all conditions of the sale are met, after which the funds and documents are transferred to the appropriate parties.

Escrow Agent: A neutral third party (individual or company) that manages the escrow process, ensuring that all aspects of the contract are fulfilled before releasing funds and documents to the relevant parties.

Lien: A legal claim against a property, often for unpaid debts such as taxes or contractor fees, that must be settled before the property can be sold.

Mortgage: A loan specifically for purchasing real estate, where the property itself serves as collateral. The lender retains an interest in the home until the loan is fully repaid.

Purchase Contract: Also known as a “purchase agreement,” this is a legal agreement between a buyer and seller outlining the terms and conditions of a home sale. It typically includes the sale price, earnest money deposit amount, and any contingencies the buyer wants to include.

Title Insurance: A policy that protects against financial loss from defects in the title to real property, such as liens or past ownership disputes. This insurance is typically required by lenders and is often purchased by the buyer or seller.

Title Search: A detailed examination of public records to confirm that the seller has legal ownership of the property and that no issues (like unpaid taxes or legal claims) could affect the sale.

Transfer of Ownership: The legal process by which property rights are passed from the seller to the buyer, usually completed by recording the deed in public records at the close of escrow.

Underwriting: The process in which a lender evaluates the risk of offering a loan to a buyer by reviewing their financial status, including credit history, income, and other factors.

Disclaimer: This is a basic overview of the real estate escrow process and timeline in California. You could encounter additional steps that are not covered above, based on the details of your transaction. The process can vary from one transaction to the next.