In the San Francisco Bay Area, home buyers often find themselves caught up in multiple-offer…

How a Home Appraisal Contingency Works in California

In California, a home appraisal contingency can give home buyers a legal exit strategy. If the home appraises below the purchase price, this contingency allows the buyer to back out of the deal without forfeiting their earnest money.

Like the other elements contained within a real estate contract, contingencies are legally binding. So home buyers should take care when using them.

In this guide: We will explain how the home appraisal contingency works, why some California home buyers use them, and how it can affect you when making an offer.

What Is a Home Appraisal Contingency?

When buying a home in California, you will have the option to include certain contingencies within your contract or purchase agreement.

In legal terms, a contingency is a future event or scenario that has to happen, in order for the real estate transaction to proceed. The sale is contingent upon this event occurring, hence the term.

In California, real estate purchase agreements can include several different types of contingencies. The home appraisal contingency is one of the most commonly used, for reasons that will soon become clear.

Definition: A home appraisal contingency is a clause in a real estate contract that allows the buyer to back out of the deal if the property’s appraised value is lower than the agreed-upon purchase price.

This means that if a professional appraiser values the house for less than what you’re offering, you can choose to walk away without losing your earnest money deposit. This is important, because lenders typically won’t give you a mortgage for more than the appraised value.

What It Means When the Appraisal ‘Comes in Low’

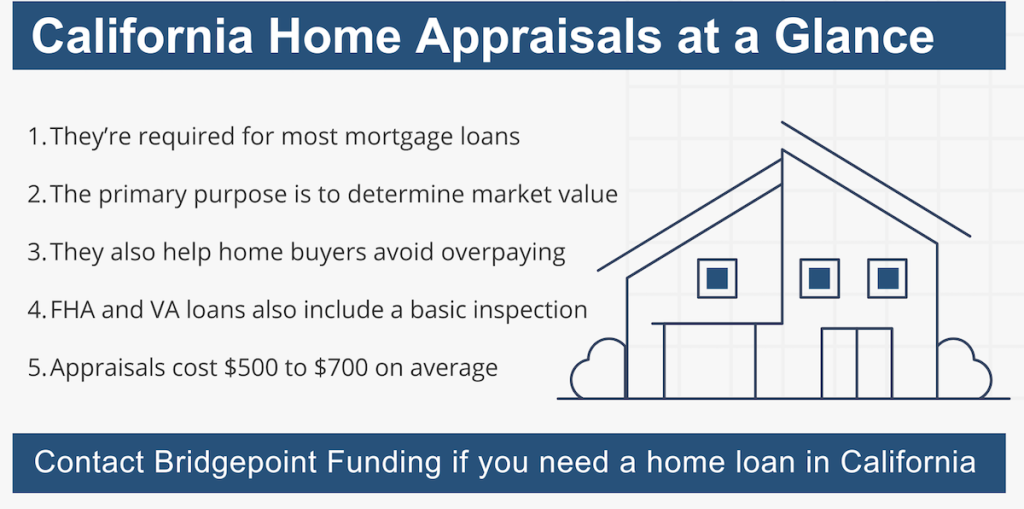

If you use a mortgage loan to buy a home in California, your lender will require a home appraisal.

A home appraisal is an estimate of a property’s fair market value. To determine the value, an appraiser will consider factors such as the home’s size, condition, location, and recent sales of comparable homes in the area.

In California, all types of mortgage loans require an appraisal. This includes conventional, FHA, and VA home loans. And the reason is always the same. The lender wants to make sure the home’s value matches (or exceeds) the loan amount.

The appraisal usually takes place after the buyer and seller have agreed on a sale price and signed a purchase agreement. At that time, the lender will order an appraisal to determine the current market value of the property.

If an appraisal comes in below the agreed-upon purchase price, a home buyer has several options. Here are the most common strategies:

- Increase your down payment: You can cover the difference between the appraised value and the purchase price with a larger down payment. This means you’ll be borrowing less money from the lender.

- Renegotiate with the seller: You can try to negotiate with the seller to lower the purchase price to match the appraised value. This might involve a new offer or a renegotiation of the original terms.

- Dispute the appraisal: If you believe the appraisal was inaccurate, you can request a second appraisal from a different appraiser. However, depending on the mortgage lender, this might not be an option.

- Walk away from the deal: As a last resort, the home buyer could terminate the contract and walk away from the deal. But this could put the earnest money deposit at risk, unless they use an appraisal contingency.

Let’s zoom in on the last resort option listed above. If you have no other choice but to back out of the deal, an appraisal contingency could prevent you from losing your deposit.

Protecting Your Earnest Money Deposit

Some home buyers in California use appraisal contingencies to protect their earnest money deposit, in case of the scenario described above.

This type of contingency allows the buyer to exit the transaction if the property appraises below the purchase price and the seller refuses to lower it.

The exact wording can vary, but it usually looks something like this:

“If the appraised value of the Property as determined by a qualified appraiser selected by the Lender is less than the Purchase Price, Buyer may terminate this Contract and receive a full refund of the Earnest Money Deposit. If Buyer elects to terminate, Buyer must provide written notice to Seller within [number] days of receiving the appraisal.”

Alternatively, a home buyer could include the actual dollar amount of the purchase price, making the clause even more specific. The buyer’s real estate agent can adjust the wording based on the specifics of the deal.

Important point: If a home buyer in California backs out of a transaction without a valid reason stated in the contract, they risk forfeiting their earnest money deposit. And that could be a costly setback.

Waiving Contingencies in a Hot Real Estate Market

Today, many of California’s real estate markets remain highly competitive due to tight inventory conditions. As a result, home buyers often have to go above and beyond to compete with other offers.

This is why some home buyers in California choose to waive their home appraisal contingency. They do this to make their offers “cleaner” and less complicated for the seller.

A cleaner offer is a more appealing one, from a seller’s perspective. In a hot market, a buyer might feel compelled to waive or omit certain contingencies, just to be competitive.

Over the past couple of years, we’ve seen an increase in the number of home buyers waiving their appraisal (and other) contingencies. But there are certain risks associated with the strategy.

The primary risk is something we’ve already covered.

If a home buyer backs out of a real estate transaction after signing a purchase agreement, and does not have the necessary contingency in place, they could end up losing their earnest money deposit.

Earnest money deposits commonly range between 1% and 3% of the purchase price. So they can easily add up to thousands of dollars, especially in pricey real estate markets.

Key Points to Take Away From This Guide

We’ve covered a lot of information in this buyer’s guide, and it’s all worth remembering. So let’s wrap up by summarizing some of the most important points.

- Definition: A home appraisal contingency allows buyers to back out if the appraised value is lower than the purchase price, while protecting their earnest money.

- Appraisal process: Lenders require an appraisal to ensure the home’s value matches or exceeds the loan amount.

- Low appraisal options: Buyers can increase their down payment, renegotiate with the seller, dispute the appraisal, or back out with an appraisal contingency.

- Waiving contingencies: In competitive housing markets, buyers will sometimes waive contingencies to make their offers more attractive.

- Legal risks: Backing out of a deal without a valid contingency could lead to the loss of the earnest money deposit.

Disclaimer: This article provides a basic overview of home appraisal contingencies in California. It’s not meant to take the place of professional legal or real estate advice. We encourage home buyers to research this topic thoroughly in order to make an informed decision when buying a house.