As a mortgage company that specializes in VA home loans, we receive a lot of…

Documents and Paperwork Needed for a VA Loan in California

This article is part of an ongoing series that explains the VA loan process in California. Today, we will cover some of the standard paperwork and documents that are required for VA home loans in California.

Here are the six most important points covered in this guide:

- VA loans are a form of government-backed mortgage program.

- The program is managed by the U.S. Department of Veterans Affairs.

- Borrowers have to provide a variety of documents when applying for a VA loan.

- Many of these documents are the same ones used for conventional (non-VA) loans.

- You’ll probably have to provide bank statements, tax returns, W-2s, and similar documents.

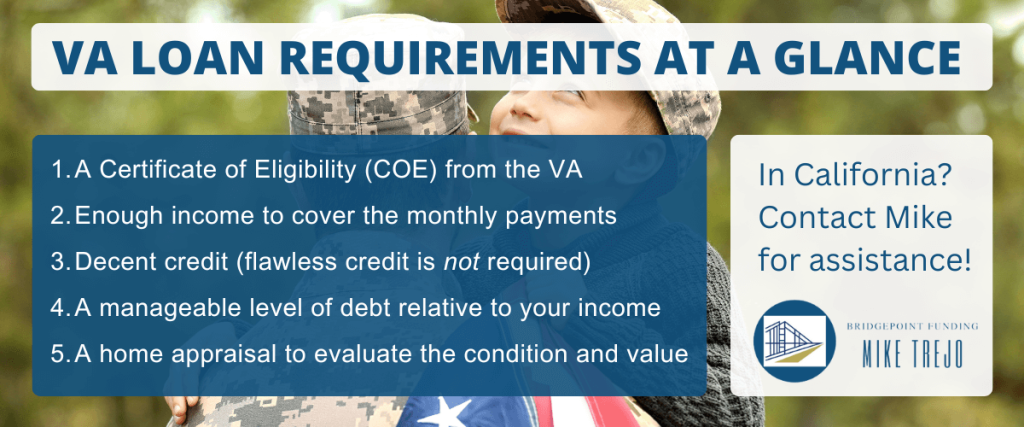

- You will also need a Certificate of Eligibility (COE), which you can request directly from the VA.

Need help? Bridgepoint Funding specializes in the VA loan program and serves borrowers across the state of California. We can assist you with every step in the process.

Documents Needed for California VA Loans

Are you a military member or veteran living in the Golden State? If so, you’re probably eligible for the Department of Veterans Affairs (VA) loan program.

This is a popular mortgage product among servicemembers and veterans, and with good reason. It allows you to buy a house with no money down, among other benefits.

As with other mortgage programs, California VA loans require certain documents from the borrower. Some of these items can be provided electronically, which simplifies the application process.

Here are the most common VA loan documents and paperwork:

- A Certificate of Eligibility (COE), obtained from the Department of Veterans Affairs. This document shows that you are eligible for the VA loan program.

- A completed “Uniform Residential Loan Application” (Fannie Mae Form 1003, or Freddie Mac Form 65). This document is required for most types of mortgage products, including VA loans.

- IRS W-2 forms (“Wage and Tax Statement”), typically for the last two years. Copies are acceptable in most cases.

- Paycheck stubs showing year-to-date earnings, usually for the past couple of months.

- Copies of bank account statements (checking and savings) for the last two or three months. These documents are used to verify your assets and cash reserves.

- IRS form 4506-T, Request for Transcript of Tax Return. This document allows the lender to obtain your tax returns directly from the IRS, for income verification purposes.

- Copies of quarterly or semiannual statements for CDs, IRA, 401(k), money markets, etc. These are also used for asset verification.

- A copy of the real estate purchase agreement / sales contract (later on, when you actually have one).

- A copy of your Social Security card if applicable, and possibly your driver’s license.

Note: This is a partial list of the most commonly requested mortgage documents for California VA loans. If you apply for a loan through Bridgepoint Funding, we’ll provide you with a complete list of required documents.

Why Lenders Require So Many Documents

Mortgage lenders ask for so many documents because they need to build a complete picture of your financial health and ensure that you meet both VA and standard lending requirements.

These documents help verify your income, assets, and overall creditworthiness, which in turn protects both you and the lender throughout the process.

Here are some key reasons for this thorough review:

1. Verification of Income and Employment

Lenders use documents like pay stubs, W-2s, and tax returns to confirm that you have a reliable and steady income. This helps ensure you can make your monthly payments.

2. Confirmation of Assets

Bank statements and investment records show your available funds for down payments, closing costs, or reserves. This verification reassures lenders that you have the financial backing needed for homeownership.

3. Compliance with VA Guidelines

Some documentation is specifically required by the VA to confirm your eligibility and to protect the integrity of the VA loan program. This is in addition to the standard documents used for other mortgage products.

4. Risk Assessment

By reviewing your complete financial history, lenders can more accurately assess the risk involved in lending you money. This helps them decide on the terms of your loan and whether you qualify.

5. Fraud Prevention

Detailed documentation makes it more difficult for fraudulent activities to occur. Having a thorough set of documents protects both you and the lender from potential risks.

6. Legal and Regulatory Requirements

Many documents are necessary to meet industry regulations and legal standards. This ensures that all parties involved are following the rules and that the loan process remains transparent and fair.

Bottom line: This extra paperwork might seem overwhelming at first. But each document plays an important role in the VA mortgage loan application, underwriting, and approval process.

Additional Paperwork for Self-Employed Borrowers

If you are currently self-employed, you might have to provide some additional paperwork when applying for a VA loan in the state of California. Additional documents required for self-employed borrowers can include the following:

- Tax returns for the most recent two years, including any schedules such as the K-1 (“Partner’s Share of Income, Deductions, Credits”).

- A copy of your profit and loss (P&L) statement with any related balance sheets.

- A copy of your corporate/partnership tax returns for the last two years, if applicable.

- Copies of any 1099 forms relating to your business.

Generally speaking, self-employed mortgage applicants can have less predictable income compared to salaried employees. So lenders need more evidence to confirm that the business is stable and that income levels are sufficient to cover monthly mortgage payments.

We are happy to answer any questions you have about California VA loan documents for self-employed borrowers. Just call or email us if you need further assistance.

When Do I Have to Provide the Documentation?

The VA mortgage process in California has several stages to it. But it all starts with application and pre-approval. This happens on the front end of the process, before you start house hunting.

As a borrower, you’ll provide most of the documents mentioned above when you first apply for a loan. The Certificate of Eligibility (COE) is the most important document at this stage, because you cannot move forward without it.

You might also encounter additional requests during the mortgage underwriting stage. Sometimes a mortgage underwriter will need additional information, documents, or explanations from the borrower.

Electronic Submission and e-Signing

Many of the documents mentioned above can be submitted electronically. Current mortgage processing technology, including electronic signatures or “e-signing,” has reduced the need for paper submission. This can make the entire process more streamlined and efficient, for borrower and lender alike.

The mortgage industry has been moving toward a more paperless, electronic process for the past few years. The coronavirus pandemic gave that transition a major push. Suddenly it became necessary — and not just convenient — to submit mortgage documents electronically.

If you choose Bridgepoint Funding as your mortgage provider, we will ensure that the VA loan document submission process goes as smoothly as possible!