When buying a home in California, or even when simply researching the process, you'll eventually…

What to Know When Buying a First Home in Los Angeles: 2025 Update

As a California-based mortgage company, we do our best to educate home buyers about real estate market trends and conditions that might affect them. We leave no stone unturned in these efforts.

This guide covers some of the most important trends first-time home buyers in Los Angeles need to know about in 2025. It covers everything from inventory levels to home prices to competition and more.

The Los Angeles-Long Beach Metro Area

We refer to the “Los Angeles area” in this report for the sake of simplicity. But the actual market statistics and trends we have compiled apply to the broader metro area as well.

This housing market update covers the Los Angeles-Long Beach-Anaheim combined statistical area (CSA), also known as “Greater Los Angeles.”

Did you know? With a population of nearly 13 million residents, the L.A. metro is the second-largest metropolitan area in the United States. It’s second only to the New York City metro in terms of population.

5 Things L.A. Home Buyers Need to Know in 2025

Are you planning to buy your first home in the Los Angeles area during 2025? If so, you’ll want to spend some time researching local market conditions in the community where you plan to buy.

Localized market research benefits first-time home buyers in the following ways:

- Helps you identify the typical price range for homes in your target area.

- Reveals whether home prices are rising, falling, or staying stable.

- Helps you choose areas that fit your lifestyle, budget, and future goals.

- Shows whether there are many homes for sale (buyer’s market) or few (seller’s market).

- Helps you recognize when a particular home is fairly priced or overpriced.

- Indicates how competitive the market is so you can navigate accordingly.

- Helps you determine how quickly (or slowly) homes are selling in your target area.

Noteworthy Trends: With that in mind, let’s look at some of the most important housing market trends that Los Angeles first-time buyers need to know about in 2025.

1. There are more homes for sale in Los Angeles in 2025.

Here’s some great news for first-time buyers. The number of active real estate listings across the Los Angeles metro area has increased significantly in recent years. This means more properties to choose from.

According to a February 2025 report from Realtor.com, active real estate listings increased by 43% over the previous 12 months. During that same timeframe, new listings increased by around 27%.

A simultaneous rise in both active and new listings suggests a cooling market. While it doesn’t necessarily indicate a buyer’s market, it does signal a shift toward more buyer-friendly conditions.

When this report was last updated in March 2025, the Los Angeles Metro area had about a four month supply of homes for sale. That was a big improvement from a couple of years ago and higher than the national average.

So, from a supply standpoint, first-time home buyers in L.A. should have an easier time finding a suitable property in 2025.

2. Home prices are higher now than last year, and still rising.

According to data from Zillow, the median home price for the Los Angeles-Long Beach-Anaheim housing market rose to $950,740 in February 2025. That was an increase of 4.3% from a year earlier.

This is arguably the biggest challenge for many first-time home buyers in the Los Angeles area. While inventory levels have become more favorable, the L.A. area continues to deal with affordability issues.

The good news is that home prices in the L.A. area are expected to level off throughout the rest of 2025. If that turns out to be true, it should ease some of the urgency among first-time buyers.

Los Angeles home buyers should also know that house prices can vary significantly from one city to the next, even within the same metropolitan area.

The L.A. area covers a broad spectrum when it comes to home values. For example, the current median price in the city of Irvine ($1,561,760) is more than double the median for Oxnard, California ($753,934). So it pays to shop around.

3. Renting a home in L.A. is cheaper than buying one in 2025.

In past years, the monthly cost difference between renting and buying a comparable home in the Los Angeles area has been fairly close. But all of that changed during the pandemic-fueled price spike.

In 2025, the latest data show that it’s significantly cheaper to rent a home in the Los Angeles area than it is to buy one.

For example, a February 2025 report from Realtor.com ranked Los Angeles among the top 10 US metros that are “becoming more renter-friendly and less buyer-friendly.”

According to that report, renters in the Los Angeles-Long Beach-Anaheim metro area spend about 36% of their income on their monthly rent. Homeowners, on the other hand, spend nearly 75% of their income on their monthly housing costs.

But the benefits of homeownership go beyond the monthly costs.

Building equity through mortgage payments provides a long-term investment, potentially leading to wealth accumulation. And fixed-rate mortgages offer predictable monthly costs, shielding homeowners from fluctuating rental prices.

Homeowners also gain the freedom to personalize their living space without landlord restrictions and establish deeper community roots, fostering a sense of stability and security.

4. Overall, the market still favors sellers over buyers.

Inventory levels within the Los Angeles real estate market have risen over the past year. That bodes well for first-time home buyers who are planning to make a purchase in 2025.

Overall, however, the L.A. metro housing market continues to favor sellers when it comes to pricing and negotiations.

Last month, only about 11% of real estate listings across the Los Angeles-Long Beach metropolitan area had a price reduction. This shows that most sellers are holding their ground when it comes to the asking price, which is indicative of a seller’s market.

But this could change over the coming months, especially if inventory levels continue to rise and/or buyer demand weakens.

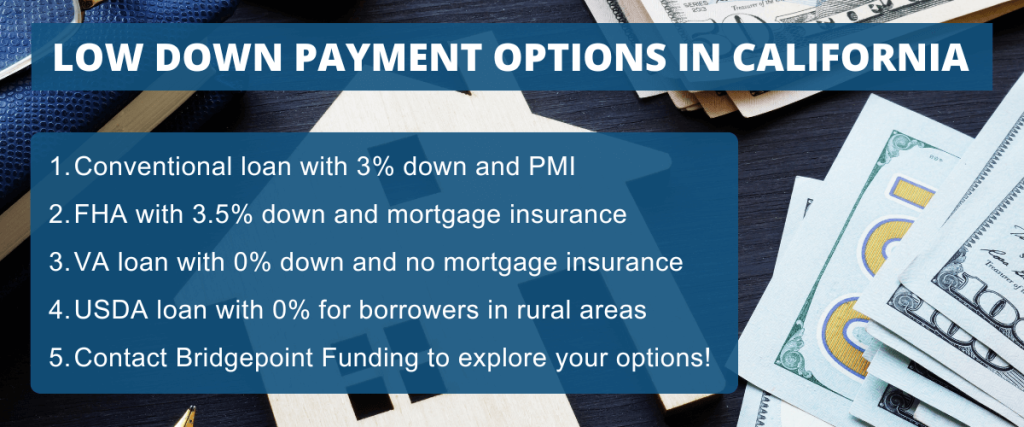

5. You have a lot of options when it comes to mortgage financing.

There’s a common misconception that first-time home buyers in Los Angeles need to make a down payment of 20% or more when buying a house.

The reality is that a lot of mortgage programs allow for a relatively low down payment, as low as 3% to 3.5% in some cases. And most of those programs allow borrowers to use money from an approved third party, such as a family member.

Additionally, military members and veterans in Los Angeles can qualify for VA mortgage financing that eliminates the need for a down payment altogether.

The point is, you have a lot of options when it comes to financing your home purchase, and you don’t necessarily have to put 20% (or even 10%) down.

Need a loan in Los Angeles? Bridgepoint Funding has been serving borrowers in the state of California for nearly 20 years. Please contact us if you have financing questions or want to apply for a loan.