Self-employment offers a lot of freedom and flexibility. But it can also pose some unique…

Fixed-Rate Second Mortgage: A Financing Option for California Homeowners

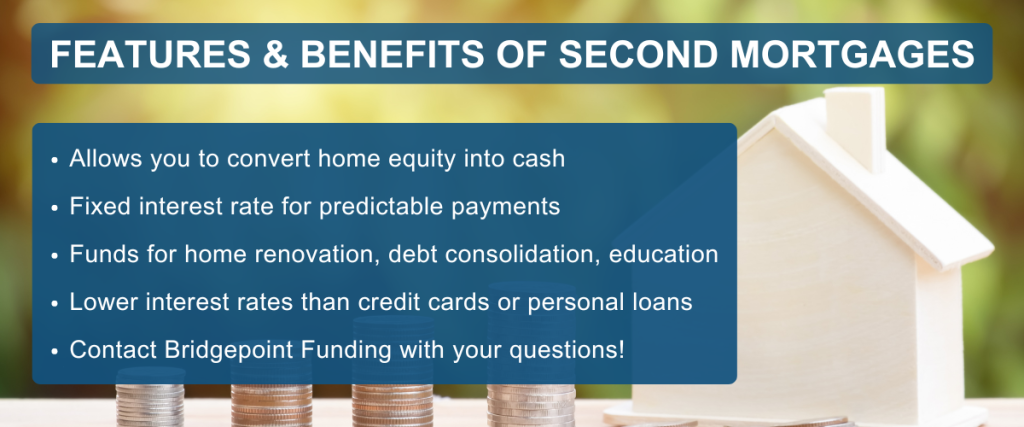

Homeowners in California have several ways to convert their home equity into cash. One common strategy is to use a second mortgage (a.k.a., home equity loan) that delivers a lump-sum payment based on the equity you’ve built up.

We recently helped a client obtain a fixed-rate second mortgage with a favorable interest rate and without the client having to pay for discount points. They were able to convert some of their equity into cash, with the benefit of a fixed interest rate on the second loan.

This guide explains what a fixed-rate second mortgage is, how the process works, and how it can benefit California homeowners who have positive equity.

What Is a Fixed-Rate Second Mortgage?

If you’re a homeowner with a mortgage loan, you already know what a “first mortgage” is. That’s the one you used when you first purchased the home. It sits in the first lien position, which means it has priority over any other liens on the property.

But some homeowners in California don’t realize that they can also take out a second mortgage loan secured by the equity in their homes. These are commonly referred to as home equity loans.

The second loan can also have a fixed interest rate, making it easier to plan and budget over the long term. This distinguishes the second mortgage from other equity-based products, such as the home equity line of credit (HELOC). HELOCs usually have a variable interest rate.

We’ll revisit this comparison in a moment. But first, let’s talk about the benefits of using a fixed-rate second mortgage from a homeowner’s perspective.

Benefits and Advantages for Homeowners

If you’ve owned a home in California for at least a couple of years, your home’s value has probably gone up. That’s because house prices in California tend to rise steadily over time, with occasional downturns that coincide with recessions.

Rising home prices help homeowners build equity, which is the difference between the amount you owe on your mortgage and the value of the property.

A fixed-rate second mortgage loan could help you convert some of that equity into cash, which you could use for a wide variety of purposes.

But that’s just one of several benefits…

- Predictable Payments: Fixed-rate mortgage products can make long-term budgeting easier, since your monthly payment stays the same over time.

- No Rate Increases: With a home equity line of credit (HELOC), your interest rate can change over time. This means your monthly payment could increase significantly. In contrast, a fixed-rate second mortgage replaces this uncertainty with predictability.

- Access to Equity: You can use your home’s value to help fund other things, such as a renovation project or a college tuition.

How You Can Use The Money

In California, there are few limits as to how you can use the funds obtained through a fixed-rate second mortgage. Homeowners use them to help fund a wide variety of projects, purchases and goals.

Here are some of the common uses for second mortgages in California:

1. Home Improvement and Renovations

This is the most popular use for home equity loans. Homeowners often use the funds for major renovation projects like kitchen or bathroom remodels, room additions, roof replacements, etc.

These renovations can also increase the property value. So you’re basically pulling cash out of the home and putting value back in, through upgrades or improvements.

2. Debt Consolidation

California homeowners with high-interest debts like credit cards or personal loans sometimes use home equity loans to pay off those debts.

Generally speaking, fixed-rate second mortgages tend to have lower interest rates than credit cards and personal loans. So by using the home equity funds to pay off those debts, a homeowner could simplify their monthly payments while reducing interest costs over time.

3. Education Expenses

A second mortgage can also help cover tuition, fees, and other education-related costs for the homeowner or their children.

4. Medical Expenses

Unexpected medical bills can create a significant financial burden. A home equity loan can provide the funds needed to cover these expenses and avoid high-interest medical debt, collections, and related problems.

5. Major Purchases

While not as common as the previous uses, home equity loans can finance large purchases like a new car, a wedding, or even a dream vacation. But some financial advisors recommend against this, since you’re using your home as collateral for a non-essential expense.

6. Real Estate Investments

Some homeowners in California use fixed-rate second mortgages to finance other real estate purchases, such as buying an investment property. This strategy uses the equity in the primary residence to secure funding for additional property investments.

But there is some risk to consider here. If the investment property doesn’t yield the expected returns, it could leave the borrower with additional debt.

Bottom line: You can use the funds provided by a fixed-rate second mortgage for a variety of purposes. But most homeowners in California use them for home renovation projects or debt consolidation.

How It Compares to a HELOC

The second mortgage is just one of several ways California homeowners can turn their equity into cash. The home equity line of credit (HELOC) also allows you to accomplish this goal, but it works differently when compared to a second mortgage.

A HELOC is a revolving credit line that uses the borrower’s home equity as collateral. Unlike the lump-sum payment method of a second mortgage, a HELOC allows homeowners to withdraw funds as needed up to a certain credit limit.

The table below compares the primary features of both financing options.

| Feature | Second Mortgage | HELOC |

| Interest Rate | Fixed | Variable |

| Payments | Predictable | Can change over time |

| Access to Funds | Lump sum at closing | Draw as needed during draw period |

| Best For | Planned expenses, stability | Ongoing/flexible needs |

Is a Fixed-Rate Second Mortgage Right for You?

The best way to choose between a HELOC and a home equity loan is to consider the purpose and goal. In other words, what do you hope to accomplish by converting your equity into cash?

Chances are, you’ll see yourself in one of the following descriptions.

Home Equity Loan: Best for one-time, large expenses with known costs, such as a major home renovation, debt consolidation, or a large purchase.

HELOC: Ideal for ongoing expenses or projects with unknown or fluctuating costs, like college tuition, a series of home improvements, or emergency funds.

Some other important questions to consider:

- Do I know exactly how much money I need?

- Do I want the stability of a fixed interest rate or the flexibility of a variable rate?

- Am I comfortable with a large upfront loan and immediate repayment, or do I prefer the flexibility to borrow as needed?

- Do I have the discipline to manage a line of credit responsibly?

Have questions? If you’re a homeowner in California looking for ways to leverage your equity, Bridgepoint Funding can help. We have access to multiple lenders and a wide range of financing options, including the popular fixed-rate second mortgage explained above.