As a home buyer in California, you have many different options when it comes to…

Why Home Appraisals Are Required for Mortgage Loans in California

Is a home appraisal required for a mortgage loan in California? This is a common question among first-time home buyers, and also a common source of confusion. So let’s clear things up!

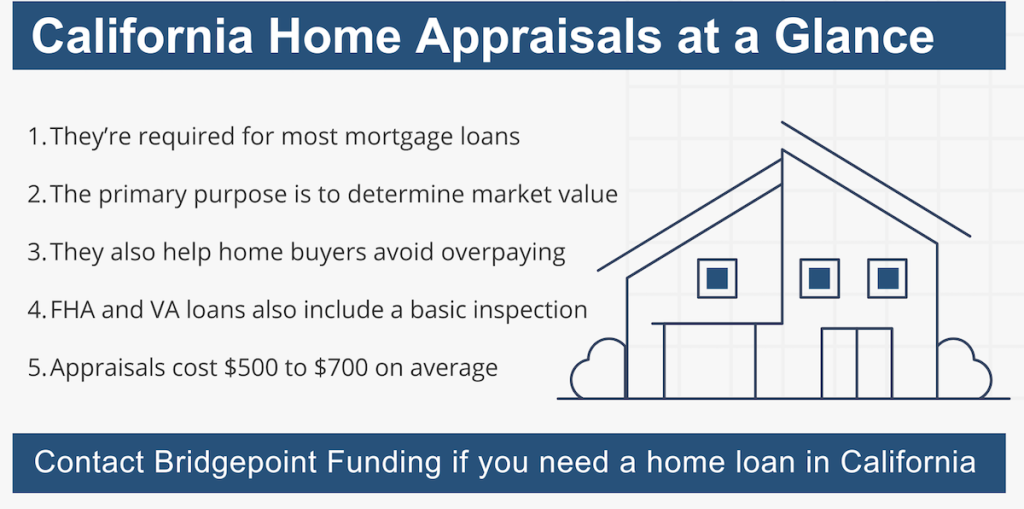

The short answer is yes. A thorough appraisal conducted by a licensed appraiser is almost always required for home loans in California. This is true for conventional, FHA, and VA loans.

What Is a Home Appraisal?

Definition: A home appraisal is an independent, professional opinion of a property’s market value.

Licensed appraisers are trained to evaluate local real estate market conditions and individual property features to determine a market value. In California, they must complete at least 150 hours of approved education courses prior to licensing.

In California, the home appraisal process usually works like this:

- Gathering data: The appraiser collects information about the property, such as size, age, overall condition, and any unique features it has.

- Researching comps: They’ll also identify comparable sales (comps), which are recent sales of similar homes in the same neighborhood.

- Analyzing the market analysis: The appraiser studies local housing market trends, including supply and demand, interest rates, and economic conditions.

- Viewing the property: The appraiser visits the property to assess its condition and any potential issues.

- Determining value: They use various methods to estimate value, such as the sales comparison approach, cost approach, and income approach.

- Reconciling results: If multiple methods are used, the appraiser will weigh the results to arrive at a final estimated value for the home.

- Preparing the report: The appraiser documents their findings and conclusions in a detailed report, which is then delivered to the lender that initially requested it.

Learn more: We have another guide that explores the appraisal process in more detail.

How It Works for Conventional Loans

A conventional mortgage loan is one that is not insured or guaranteed by the federal government. The conventional label distinguishes these “regular” home loans from programs such as FHA and VA, which do receive government backing.

Key point: In California, home appraisals are usually required for conventional mortgage loans. The appraiser’s report gives the mortgage lender better insight into the actual market value of the home.

Conventional loans are commonly sold into the secondary mortgage market through Fannie Mae and Freddie Mac. These government-sponsored enterprises (GSEs) purchase loans from lenders, securitize them, and then sell them off to others investors.

But both Fannie and Freddie have specific requirements for the loans they purchase, and a home appraisal is one of those key requirements.

As it states on the Freddie Mac website: “Freddie Mac requires that the [mortgage] Seller obtain an appraisal report that accurately reflects the market value, condition and marketability of the property.”

They go on to define the market value as: “The most probable price which a property should bring in a competitive and open market under all conditions requisite to a fair sale…”

Bottom line: If you use a conventional loan to buy a house in California, an appraisal will probably be required. And as the borrower, you’ll likely be the one who pays for it.

How It Works for FHA and VA Loans

Government-backed mortgage programs usually have an appraisal requirement as well. This is true for both the VA and FHA home loan programs, the two most popular types of government-backed mortgages.

Home appraisals are required for all FHA loans in California, and for a couple of reasons. The primary reason is to determine the value of the house, as we discussed in the previous section.

But with an FHA-insured mortgage loan, the appraiser must also review the condition of the home, to ensure it meets all requirements set forth by the Department of Housing and Urban Development (HUD).

The same is true for VA loans, which are popular among military members and veterans. In California, a home appraisal is nearly always required for VA-guaranteed mortgage loans.

Key takeaway: Unlike a conventional home appraisal, which mainly focuses on the property’s market value, an FHA or VA appraisal will also evaluate the home’s overall condition.

Why Appraisals Are Required

We talked about the primary purpose for the home appraisal. The appraiser is trying to determine how much a particular property is worth, based on current conditions within the real estate market.

They will examine the home in question and compare it to others that have sold recently within the same area. In doing so, the appraiser can come up with an educated guess as to the home’s current market value.

In California, mortgage lenders usually require home appraisals as part of the loan review and underwriting process. It’s a common requirement and also an industrywide standard.

Lenders carry a certain amount of risk when offering home loans to borrowers. The lender is often the one providing most of the funds. For example, if a borrower puts 20% down, the lender is funding the remaining 80%.

That’s why most mortgage lenders in California require an appraisal. It helps them make wise lending decisions and protect their investment, while adhering to the rules from secondary organizations like Freddie Mac, Fannie Mae, or FHA.

It all boils down to one thing. Home appraisals are required for nearly all California home loans.

The Home Buyer’s Role in All of This

As a home buyer in California, you won’t have an active role in the appraisal process. You might have to pay for it, which is customary. Buyers usually foot the bill. But there’s not much for you to do at this stage, other than “wait and see.”

The appraiser will evaluate the property, coordinating with the homeowner to gain access. The appraiser will then conduct a thorough review of comparable sales in the area, to get to a point of comparison.

Finally, they will issue an appraisal report with the estimated market value of the property in question. This report is delivered to the mortgage lender and usually ends up in the loan file.

But aside from paying for the appraisal, the home buyer has a limited role in this process.

Other Common Mortgage Requirements

A mortgage loan is a major financial undertaking. Because of this, banks and mortgage lenders impose certain requirements and criteria for borrowers. Home appraisals are just one of those requirements.

Additionally, some home loan rules and requirements are passed down by secondary authorities such as the Federal Housing Administration or Freddie Mac. These organizations purchase, guarantee, or insure the mortgage loans made by lenders in the private sector. So they have their own requirements as well.

Common requirements when taking out a home loan include:

- A good credit score, but not necessarily perfect

- A manageable level of monthly debt

- Sufficient income to manage the monthly mortgage payments

- Documentation relating to income, assets, and other financial factors

- A professional appraisal to determine the value of the property

These aren’t the only home loan requirements, just some of the most important ones. Depending on the type of mortgage you use and other factors, you might encounter additional criteria as well.

Have questions? Please contact us if you have questions about home appraisal requirements for mortgage loans in California, or other financing-related questions. We look forward to helping you!